These 4 Measures Indicate That Old Dominion Freight Line (NASDAQ:ODFL) Is Using Debt Reasonably Well

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Old Dominion Freight Line, Inc. (NASDAQ:ODFL) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Old Dominion Freight Line

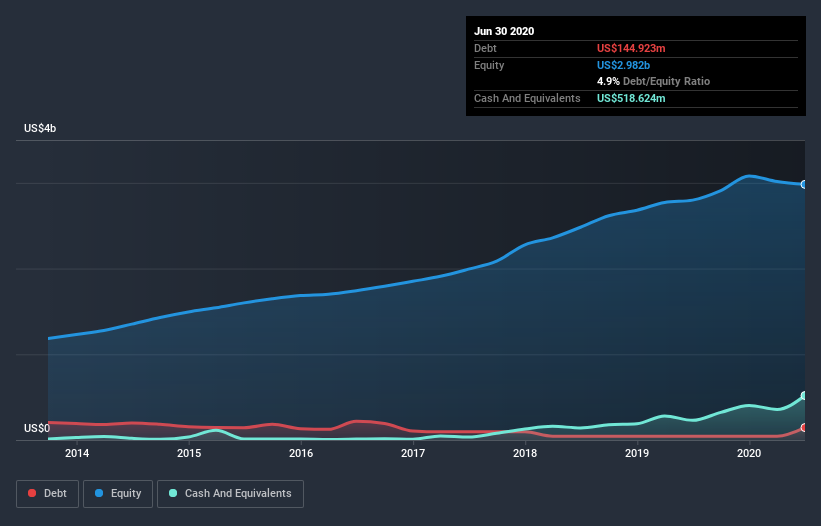

What Is Old Dominion Freight Line's Debt?

As you can see below, at the end of June 2020, Old Dominion Freight Line had US$78.4m of debt, up from US$45.0m a year ago. Click the image for more detail. However, it does have US$518.6m in cash offsetting this, leading to net cash of US$440.2m.

A Look At Old Dominion Freight Line's Liabilities

We can see from the most recent balance sheet that Old Dominion Freight Line had liabilities of US$494.2m falling due within a year, and liabilities of US$603.4m due beyond that. On the other hand, it had cash of US$518.6m and US$449.9m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$129.0m.

This state of affairs indicates that Old Dominion Freight Line's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it's hard to imagine that the US$21.5b company is struggling for cash, we still think it's worth monitoring its balance sheet. While it does have liabilities worth noting, Old Dominion Freight Line also has more cash than debt, so we're pretty confident it can manage its debt safely.

On the other hand, Old Dominion Freight Line saw its EBIT drop by 8.4% in the last twelve months. That sort of decline, if sustained, will obviously make debt harder to handle. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Old Dominion Freight Line's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. Old Dominion Freight Line may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last three years, Old Dominion Freight Line produced sturdy free cash flow equating to 50% of its EBIT, about what we'd expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing up

We could understand if investors are concerned about Old Dominion Freight Line's liabilities, but we can be reassured by the fact it has has net cash of US$440.2m. So we don't have any problem with Old Dominion Freight Line's use of debt. Of course, we wouldn't say no to the extra confidence that we'd gain if we knew that Old Dominion Freight Line insiders have been buying shares: if you're on the same wavelength, you can find out if insiders are buying by clicking this link.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.