Can Mako Gold (ASX:MKG) Afford To Invest In Growth?

Just because a business does not make any money, does not mean that the stock will go down. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. But while the successes are well known, investors should not ignore the very many unprofitable companies that simply burn through all their cash and collapse.

Given this risk, we thought we'd take a look at whether Mako Gold (ASX:MKG) shareholders should be worried about its cash burn. In this report, we will consider the company's annual negative free cash flow, henceforth referring to it as the 'cash burn'. We'll start by comparing its cash burn with its cash reserves in order to calculate its cash runway.

View our latest analysis for Mako Gold

How Long Is Mako Gold's Cash Runway?

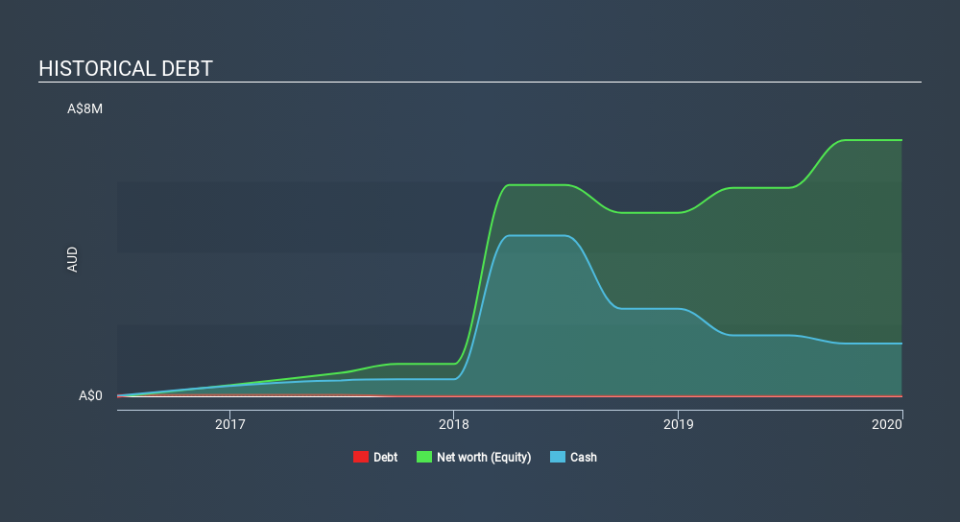

A company's cash runway is calculated by dividing its cash hoard by its cash burn. When Mako Gold last reported its balance sheet in December 2019, it had zero debt and cash worth AU$1.5m. Looking at the last year, the company burnt through AU$3.7m. That means it had a cash runway of around 5 months as of December 2019. That's a very short cash runway which indicates an imminent need to douse the cash burn or find more funding. The image below shows how its cash balance has been changing over the last few years.

How Is Mako Gold's Cash Burn Changing Over Time?

Mako Gold didn't record any revenue over the last year, indicating that it's an early stage company still developing its business. Nonetheless, we can still examine its cash burn trajectory as part of our assessment of its cash burn situation. Over the last year its cash burn actually increased by 16%, which suggests that management are increasing investment in future growth, but not too quickly. That's not necessarily a bad thing, but investors should be mindful of the fact that will shorten the cash runway. Admittedly, we're a bit cautious of Mako Gold due to its lack of significant operating revenues. We prefer most of the stocks on this list of stocks that analysts expect to grow.

How Easily Can Mako Gold Raise Cash?

Given its cash burn trajectory, Mako Gold shareholders should already be thinking about how easy it might be for it to raise further cash in the future. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. Commonly, a business will sell new shares in itself to raise cash to drive growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Mako Gold's cash burn of AU$3.7m is about the same as its market capitalisation of AU$3.5m. Given just how high that expenditure is, relative to the company's market value, we think there's an elevated risk of funding distress, and we would be very nervous about holding the stock.

How Risky Is Mako Gold's Cash Burn Situation?

As you can probably tell by now, we're rather concerned about Mako Gold's cash burn. In particular, we think its cash burn relative to its market cap suggests it isn't in a good position to keep funding growth. And although we accept its increasing cash burn wasn't as worrying as its cash burn relative to its market cap, it was still a real negative; as indeed were all the factors we considered in this article. Looking at the metrics in this article all together, we consider its cash burn situation to be rather dangerous, and likely to cost shareholders one way or the other. Taking a deeper dive, we've spotted 6 warning signs for Mako Gold you should be aware of, and 3 of them are concerning.

Of course Mako Gold may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.