They bought their home in March 2022. Why this Ontario couple calls the purchase a nightmare

Fernanda Santos and Gustavo Pereira of London, Ont., knew the housing market was wildly overpriced in March 2022, but felt pressured to become owners, so they bought a three-bedroom home in the east end for $730,000.

"Everybody said to us you should buy as soon as you can — doesn't matter if you like it or not, just buy and get into the market," Santos, 34, recalled in an interview with Rebecca Zandbergen, host of CBC Radio's London Morning.

The couple moved to Canada from Brazil in 2019 for a better life. Today, they're sitting on a mortgage with a variable rate (currently at 5.6 per cent) on a house that has fallen in value by an estimated $150,000, and paying $4,400 a month — $1,600 more than they had anticipated.

"That's not what we dreamed about," said Santos. "It's just been a nightmare for us."

In an attempt to tackle inflation, the Bank of Canada has raised interest rates eight times since the start of 2022. The central bank's rate is now at 4.5 per cent.

As well, housing prices have dropped considerably since the couple bought their home. In fact, sales in January were the lowest for that month since 2009, down 37.1 per cent compared with a year ago, the Canadian Real Estate Association (CREA) said this week.

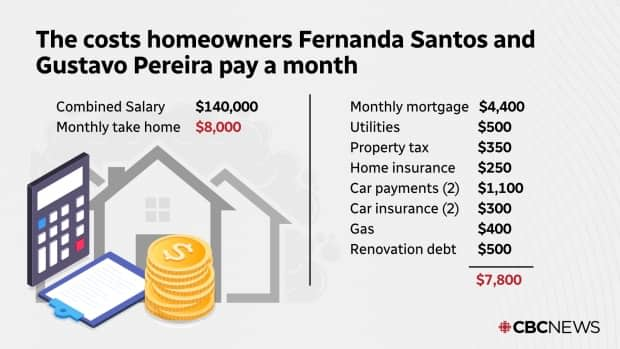

How the books of Fernanda Santos and Gustavo Pereira look each month:

"They're just going to raise the rates until they reach a point that they are comfortable with," said Santos. "But they don't think about all the people that they are impacting with that."

Despite both having good jobs, with a combined annual salary of $140,000, Santos and Pereira are struggling to keep up. Both worked as engineers in Brazil. Santos is now a senior estimator with a construction company in London and Pereira is an engineer in training.

"It's not only the mortgage," said Santos. "We have property taxes. It's a huge chunk every single month. We have insurance for the house, insurance for ourselves. So there is a lot of hidden costs."

The couple are also paying $500 a month towards the cost of home renovations.

On the weekends, the couple's work isn't done. Both drive for UberEats and Instacart in an effort to offset their bills.

"When you have like 60 per cent of your full income going toward your mortgage, you pretty much don't have anything left, plus we have to eat, right?" said Santos.

Santos and Pereira are also using their savings — money they diligently set aside for a rainy day — to buy their groceries.

Advice for homeowners feeling the pinch

Housing analyst John Pasalis, president and a broker at Toronto's Realosophy Realty Inc., said the couple should go back to their lender (in this case, RMG Mortgages) to see if they can negotiate a lower payment.

One option may be to lengthen the amortization — the amount of time it takes to pay the mortgage off in full — which can come with smaller monthly payment options.

"I think people are reluctant to do that [negotiate], but they need to push," said Pasalis, adding that lenders seem interested right now in "dampening the shock" of ballooning mortgage payments.

According to Pasalis, many variable-rate mortgage holders are not actually paying more each month.

"The majority of banks do not really increase your payments on your variable mortgage as rates go up," he said. "Most of them have fixed payments."

In those cases, more of a person's mortgage payment goes toward the interest and not the principal, which effectively extends the life of the mortgage.

For now, Santos and Pereira have put their plans to grow their family on pause.

"We had plans in the next couple years, but I can't go on maternity leave right now," she said. "If I go on maternity leave, we won't pay the bills."