CRA paid out $37M to tax scammers, unsealed affidavit alleges

A once-sealed affidavit filed with the Tax Court of Canada and obtained by The Fifth Estate details how alleged scammers tricked the Canada Revenue Agency and made off with $37 million of taxpayers' money.

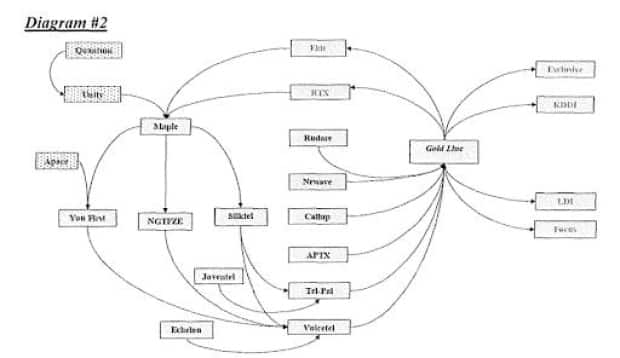

In the document, a litigation officer with the Canada Revenue Agency alleges that Toronto-area company Gold Line Telemanagement made "material misstatements" on tax returns and was "part of a group of companies that participated in sham transactions."

The affidavit, which lawyers at KPMG said could cause "irreparable harm" to Gold Line if it was released, was kept off the public record for 10 months.

After a petition to the court from The Fifth Estate, KPMG eventually reversed its position late last year and said its client would no longer oppose the release.

In its own court filings, Gold Line has rejected CRA allegations, stating "there was no deceit, intentional or otherwise," in its filings and that it was genuinely engaged in the long-distance telecom business.

Gold Line has been in the telecom business for decades, selling prepaid long distance telephone cards and other services.

The CRA alleges that starting in 2016 Gold Line acted as a middle party in the world of wholesale telecom, purporting to buy and sell international telephone call minutes. Based on what the CRA now alleges were "sham" transactions, the company claimed — and received — $37 million in sales tax refunds.

Some of the companies in Gold Line's supply chain are alleged to have participated in a separate case reported on by The Fifth Estate late last year. In that instance, the CRA admits it paid out more than $63 million in what it now calls "illegitimate" tax refunds.

WATCH | The "Swindling the System" from The Fifth Estate:

Between these two cases, the CRA claims to have wrongly dispersed $100 million to carousel schemes, a type of fraud that has been well-known to Canadian tax authorities for many years.

Also known as "missing trader fraud," carousel schemes rely on complicated supply chains filled with fake companies and invoices to create the appearance that legitimate business transactions are taking place. The companies then submit bogus tax refund claims that are paid out by unwitting governments.

"How much do you have to lose before you realize that your tax system might be vulnerable?" Mike Cheetham, a Dubai-based tax fraud analyst, said in an interview. "If I have to put the blame anywhere, it's all squarely and fairly on the CRA."

Cheetham has previously appeared as an expert witness before European Union committees regarding carousel schemes. He said other countries have implemented a "reverse charge mechanism" to sectors prone to carousel fraud, like telecom and precious metals trading — something Canada has not done.

With a reverse charge mechanism in place, certain industries are exempted from collecting sales taxes, in order to prevent bogus refunds.

"It would take a single paragraph of text in the legislation" to inhibit this kind of fraud, Cheetham said, adding that there are "20 years of milestones in Europe proving it works."

He said that without these kinds of changes, Canada's tax system is wide open for abuse.

"I will bet there's another five or 10 cases that haven't yet been discovered underway now as we speak."

Federal Revenue Minister Marie-Claude Bibeau did not respond to an email from The Fifth Estate asking why the federal government has not implemented the kind of preventive measures taken more than a decade ago in Europe.

In January, Gerald Soroka, the Conservative member of Parliament for the Yellowhead riding, west of Edmonton, asked the government in writing for an estimate of how much unwarranted money the CRA has paid out as a result of carousel schemes.

Bibeau responded that the CRA was "unable to provide the information" because "there is no systematic way to estimate the amount of all unwarranted payments."

Previous filings made in the case, and not under seal, state that while KPMG provided Gold Line with external "accounting support" and audited its financial statements, it did not prepare the GST returns at issue.

Today, KPMG Law, the legal branch of the firm, represents Gold Line in tax court.

In a statement, KPMG said that "due to client confidentiality," it cannot provide comment on the case.

Gold Line also said that as the matter is before the courts, it had been advised not to comment.

'Sham' transactions

According to a CRA analysis, Gold Line sold 10 million more minutes than it purchased. But as an intermediary, Gold Line's sales and purchases should be relatively equal, it said.

"There is overwhelming evidence that Gold Line was colluding with its suppliers and customers to deceive the CRA" the once-sealed affidavit states.

The CRA alleges the company was either knowingly involved in the scheme or "grossly negligent," noting that Gold Line did business with Canadian suppliers that were not registered to collect GST or HST, didn't have proper telecom licences, "had no business location, had no telecommunications experience and had no employees other than the shareholder/director."

Based on this and a number of other factors, the CRA concluded that "the purchase and sales transactions are sham."

The case is ongoing in the Tax Court of Canada and Gold Line argues that the tax credits it claimed were entirely based on taxes it paid to its Canadian suppliers.

Other companies in the supply chain have also gone to court to deny the CRA's allegations, none of which have been tested in court. It is possible that some intermediaries in carousel schemes can be caught up unwittingly.

If you have any tips on this story, please email in confidence Matthew.Pierce@cbc.ca or Harvey.Cashore@cbc.ca or call 416-526-4704.