Euro-Zone Activity Slows on French Vote Risk, Factory Slump

(Bloomberg) -- The rebound in euro-area private-sector business activity unexpectedly lost momentum as France’s snap election weighed on firms and manufacturing in the region recorded its worst month of the year.

Most Read from Bloomberg

CDK Hackers Want Millions in Ransom to End Car Dealership Outage

Russia Is Storing Up a Crime Wave When Its War on Ukraine Ends

Dubai Real Estate’s Resilience May Signal End of Boom-Bust Cycle

Wall Street’s Smart-Trade Brigade Thrashed Again on Stock Boom

Private Jets and Yachts Land in Nantucket for Jefferies Takeover

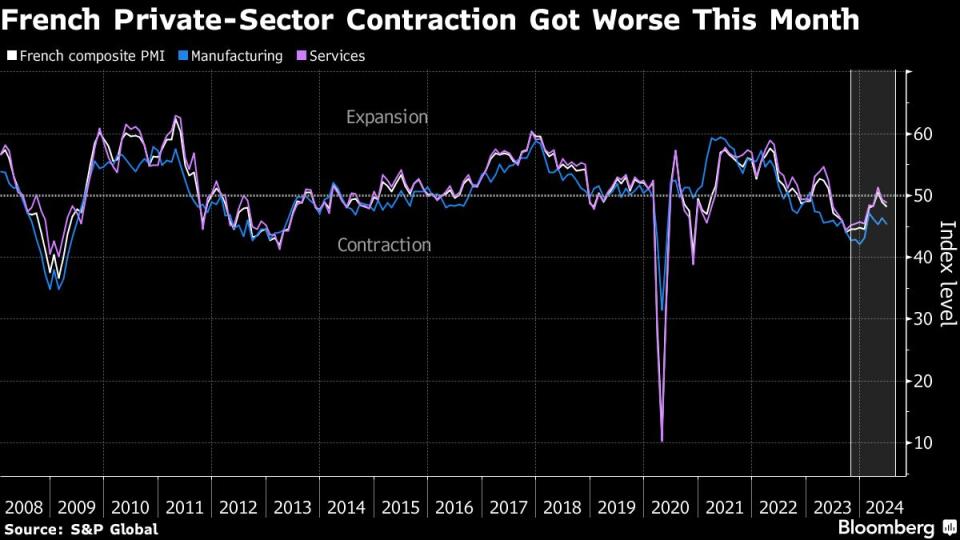

S&P Global’s composite Purchasing Managers’ Index fell to 50.8 in June. While that’s a fourth straight reading above the 50 threshold that signals growth, analysts polled by Bloomberg had predicted an advance to 52.5.

Europe’s economy remains in the early stages of a recovery from last year’s mild recession. But while growth surpassed expectations in the first quarter, recent data have suggested momentum may be waning. What’s more, President Emmanuel Macron‘s shock announcement to call snap elections has brought the prospect of a radical change in government in the region’s second-biggest economy.

“This unexpected turn of events has likely stirred up a lot of uncertainty about future economic policies, causing many companies to hit the brakes on new investments and orders,” Cyrus de la Rubia, chief economist at Hamburg Commercial Bank, said Friday in a statement.

“In any case, it is evident that France’s poor economic performance has significantly contributed to the deteriorating economic conditions in the euro zone,” he said, predicting gross domestic product in the 20-nation bloc will rise 0.2% in the second quarter.

The weaker-than-expected figures encouraged bets on interest-rate cuts from both the European Central Bank and the Bank of England. Money markets now imply 44 basis points of easing in the euro area through the end of the year, from 42 basis points before the data, and are virtually pricing two full quarter-point cuts in the UK.

Bonds gained across the board, with the yield on 10-year German notes falling as much as seven basis points to 2.36%. The euro reversed modest gains to fall 0.3% to $1.0671.

What Bloomberg Economics Says...

“The euro-area economy still appears to be recovering, despite the composite PMI unexpectedly slipping in June. Inflation is decelerating and that should continue to revive real incomes, allowing GDP growth to remain buoyant.”

-David Powell, senior economist. For full react, click here

“Flash PMIs for June suggest that the eurozone’s growth momentum is still weak,” said Leo Barincou of Oxford Economics. “Today’s PMIs do not call into question our view that the euro-zone economy will post another moderate expansion in the second quarter, but they are a downside risk for the rest of the year if momentum does not improve.”

Manufacturing Woes

A key challenge is manufacturing, with the figures from S&P — based on surveys conducted June 12-19 — dashing hopes that struggling factories are finding their feet. German industry continues to be a weak spot, with the decline there reversing some of May’s improvement. France saw a similar trend, though its malaise isn’t quite as bad.

“The services sector continues to keep the euro zone afloat,” de la Rubia said. “Even though activity didn’t pick up as much as last month and fell short of what most analysts were expecting, the overall expansion was solid.”

Help is on the way from lower borrowing costs. The European Central Bank began cutting interest rates from record levels this month and should make further reductions if inflation moderates further toward its target.

With gains in workers’ wages still elevated, markets are fully pricing just one more quarter-point cut this year, bringing the deposit rate to 3.5%. ECB President Christine Lagarde has cautioned that consumer-price growth won’t return smoothly to 2%.

“We do have plenty of challenges, but I really believe that we are now heading toward a disinflationary path that will have its little hiccups here and there — what we call bumps on the road,” she said last week.

It’s hoped that cooling inflation and falling interest rates will swell consumers’ contribution to Europe’s rebound. De la Rubia warned, however, of dangers to the disinflation process, including a steeper rise in selling prices at German service providers and the first increase in euro-area manufacturing input costs since February 2023.

“The PMIs do not provide ammunition for another rate cut in July by the ECB,” he said.

In Japan, PMI numbers also pointed to weaker activity, with the services gauge registering a contraction for the first time in almost two years. UK figures also softened, pointing to slower growth in June. US is due to publish is readings later on Friday, and is expected to stay well above 50.

PMIs are closely watched by markets as they arrive early in the month and are good at revealing trends and turning points in an economy. A measure of breadth of changes in output rather than depth, business surveys can sometimes be difficult to map directly to quarterly GDP.

--With assistance from Joel Rinneby, Mark Evans and Aline Oyamada.

(Updates with BE after seventh paragraph)

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.