Benign Growth For RADCOM Ltd. (NASDAQ:RDCM) Underpins Its Share Price

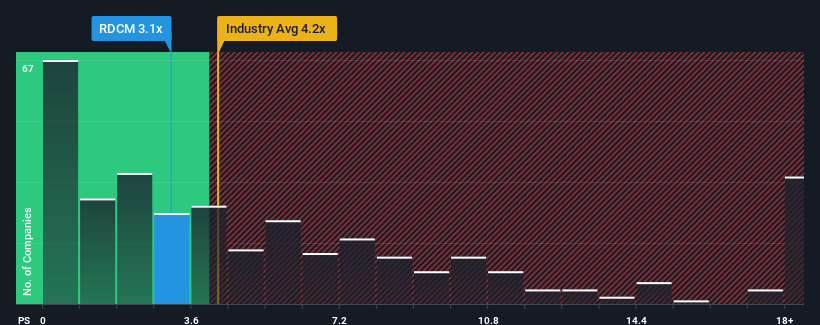

With a price-to-sales (or "P/S") ratio of 3.1x RADCOM Ltd. (NASDAQ:RDCM) may be sending bullish signals at the moment, given that almost half of all the Software companies in the United States have P/S ratios greater than 4.2x and even P/S higher than 9x are not unusual. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for RADCOM

What Does RADCOM's P/S Mean For Shareholders?

There hasn't been much to differentiate RADCOM's and the industry's revenue growth lately. One possibility is that the P/S ratio is low because investors think this modest revenue performance may begin to slide. Those who are bullish on RADCOM will be hoping that this isn't the case.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on RADCOM.

How Is RADCOM's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as low as RADCOM's is when the company's growth is on track to lag the industry.

If we review the last year of revenue growth, the company posted a worthy increase of 14%. This was backed up an excellent period prior to see revenue up by 40% in total over the last three years. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Turning to the outlook, the next year should generate growth of 10% as estimated by the dual analysts watching the company. With the industry predicted to deliver 13% growth, the company is positioned for a weaker revenue result.

With this in consideration, its clear as to why RADCOM's P/S is falling short industry peers. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Final Word

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As expected, our analysis of RADCOM's analyst forecasts confirms that the company's underwhelming revenue outlook is a major contributor to its low P/S. Shareholders' pessimism on the revenue prospects for the company seems to be the main contributor to the depressed P/S. It's hard to see the share price rising strongly in the near future under these circumstances.

Having said that, be aware RADCOM is showing 3 warning signs in our investment analysis, and 1 of those can't be ignored.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here