Saving for your kids' education: A cautionary tale

What better investment could there be than socking away money for your children's education? Even the smallest contributions can trigger free government money and create a fund to help ease the cost of a post-secondary education.

But a Calgary family is warning others about the risks of group RESPs and how a decision to leave their plan early could cost them thousands of dollars.

Hamed Hendizadeh opened two plans for his daughters with Canadian Scholarship Trust, an Ontario-based foundation that says it manages over $4.8 billion in assets for more than 250,000 Canadian families.

Hendizadeh, who is an engineer, has been contributing $400 every month to the two plans. His contributions have already climbed to $8,000 — and his daughters, Elika, 4, and Liana, 19 months, are still preschoolers.

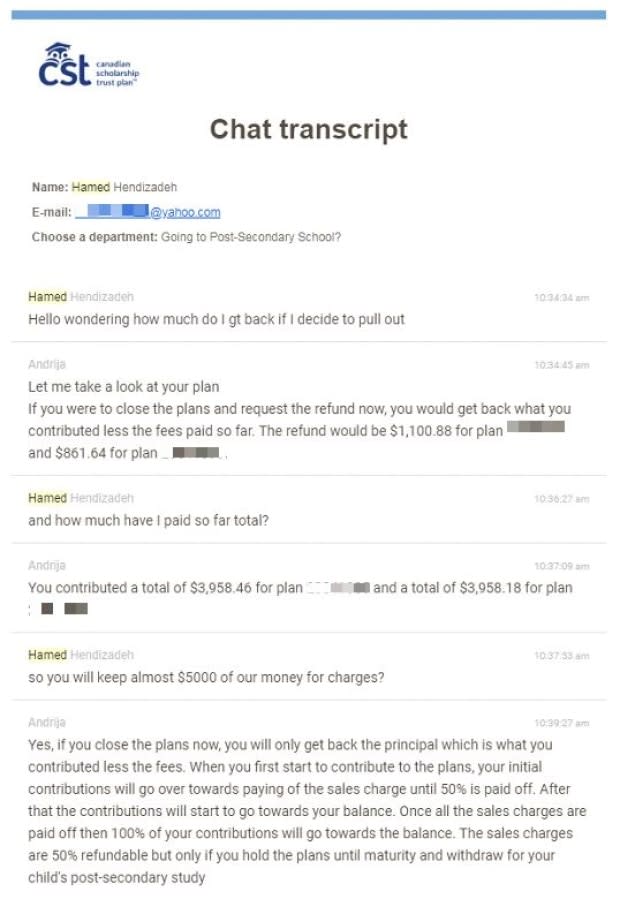

What he didn't know is that most of those contributions have been going toward the sales charges for the plans, rather than the actual Registered Education Savings Plan investment.

So, it came as a shock when he inquired about leaving the plan and the amount of money he would get back.

A representative of the foundation told Hendizadeh in an online chat that he would receive only $2,000 if he pulls out.

"This whole sales charge, I came to know about it two weeks ago," said Hendizadeh.

He says he now faces the prospect of losing $6,000 of his investment.

"This $6,000 doesn't make sense to me. I was told to go through the complaint, [the] 1-800 number," he said.

Peter Lewis, Canadian Scholarship Trust's vice-president of sales, says he could not comment on the specifics of the Hendizadeh matter but told CBC News he is proud of his company's transparency around the fees that it charges for all of its products, including group RESPs.

"We're very upfront about what those fees are and we try to very carefully explain to families that's one of the risks that you're going to take with this plan, is that you're locking into a schedule. And if it's not something you're comfortable with, then you shouldn't actually do that," said Lewis.

"Our goal is not to help families start a savings plan. Our goal is to help families finish their savings plan and get their kids to school," he said.

The company's website says it paid students $166 million for their post-secondary education last year.

Complaints not uncommon

Credit counselling agencies and financial educators say they've heard from several people who have raised similar concerns about group RESPs.

They say the plans can be confusing and complicated for new parents.

They say people should realize the product is different than an individual RESP account that is offered at banks, mutual fund companies and credit unions. With a group RESP, people are entering into a long-term contract with a specific contribution schedule that could last up to 18 years.

Jeff Loomis is the executive director of Momentum, a local organization that, among other things, teaches financial literacy to Calgarians. He says they often use the example of a cellphone contract to help explain the risks associated with a group RESP.

"Would you really want to sign up for a cellphone contract for 18 years? Because you just don't know what your future would be like 10, 12, 15 years out," Loomis said.

"So, because it's a contract and there's not a lot of flexibility, it can lock people in. So it's really important to understand that contract and ask all the questions to be an informed consumer, he said.

The Credit Counselling Society, a non-profit group, says parents need to really go through all of the material before signing a contract — and people should know that there is a 60-day window to pull out of an agreement, even after they've signed on the dotted line.

The agency says many new parents face financial and emotional stress associated with bringing a baby into the family.

"I would recommend people don't rush into getting RESPs right away, regardless. Take some time, get yourself back on a level playing field," said Mark Kalinowski.

Hendizadeh says a sales person from the Canadian Scholarship Trust visited their home just days after they brought their second daughter from the hospital and he says they were made to feel guilty for not starting the plan earlier.

"I remember we had a discussion about my first daughter and how we didn't start this for her, we were told 'it's a little bit, you should have done this two years ago,'" he recalled.

"[They] kinda want to make you feel guilty," he said.

Hendizadeh says they agreed to start the plan right away for both of his kids — something he now regrets.

"Unless you are 100 per cent sure you want to stay with them for 15 years or whatever, do not do this," he said.

"Be aware of this big commitment," he added.

Hendizadeh says the foundation has declined his request to get all of his money back, but he says the company has told him it's looking into his complaint and will have a final response next month.

Got a story idea or tip? Contact Bryan Labby at bryan.labby@cbc.ca.